Introduction

Many people in India check their credit score when they plan to apply for a loan or credit card. One common question that comes up is how often CIBIL score is updated. Someone may pay a credit card bill today and expect the score to improve immediately. But that is not how the system works.

Your CIBIL score changes only when lenders report new information to credit bureaus like TransUnion CIBIL. This includes credit card payments, loan EMIs, missed payments, and new credit applications. Because of this reporting process, score updates do not happen daily.

Understanding how often the score updates helps you manage your credit better and avoid confusion when your score does not change immediately after a payment.

This guide explains the CIBIL score update cycle in India, why delays happen, and what borrowers should do if their score is not changing.

Quick Answer: How Often CIBIL Score Is Updated

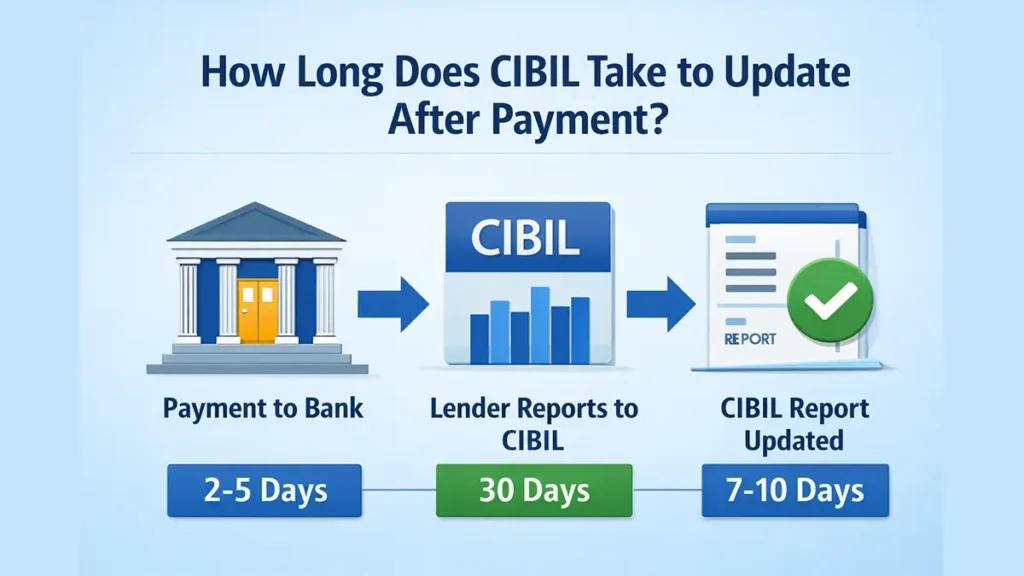

CIBIL scores in India are generally updated every 30 to 45 days after lenders submit credit data to bureaus.

This happens when banks and financial institutions submit your latest credit activity to credit bureaus like TransUnion CIBIL. Once the lender reports the updated data, the credit bureau recalculates your credit score.

Because lenders report data monthly, the score does not update instantly after you make a payment.

How the CIBIL System Works in India

To understand how often CIBIL score is updated, you must understand how the credit reporting system functions.

In India, credit scores are managed by credit bureaus that collect data from lenders.

Key players in the system

- Banks and NBFCs

- Credit bureaus

- Borrowers

The process works like this:

- You take a loan or credit card.

- Every month the bank records your payment behaviour.

- The bank sends that information to credit bureaus.

- The credit bureau updates your credit report.

- Your CIBIL score is recalculated based on the new data.

This is why your score depends heavily on how regularly lenders send updates.

What information lenders report

Banks usually report the following data:

- Credit card outstanding balance

- EMI payments

- Late or missed payments

- Loan closures

- New loan accounts

- Credit limit usage

Each update can change your credit score.

Why CIBIL Score Updates Usually Take 30–45 Days

Many people expect their score to change immediately after they pay a bill. In reality, the update depends on when the lender submits data.

Monthly reporting cycle

Most lenders follow a monthly reporting cycle. They send updated information to credit bureaus once every billing cycle.

For example:

| Activity | When it happens |

|---|---|

| Credit card bill generated | 5th May |

| Payment made | 10th May |

| Lender sends update to bureau | End of May |

| Score updated | Early June |

So even though you paid on time, the system reflects the change only after the lender reports it.

Reasons for delay

Score updates may take longer because of:

- Bank reporting delays

- Technical processing time

- Weekends or holidays

- Multiple lenders reporting at different times

This is completely normal.

How Often CIBIL Score Is Updated After Credit Card Payment

When you pay your credit card bill, the change does not appear in your credit report immediately. Many borrowers assume the score will update the next day, but that is not how the credit reporting system works.

In most cases, lenders send updated account information to credit bureaus once every billing cycle. This means your payment may reflect in your credit report after 30 to 45 days, depending on when the bank submits the data.

For example, if your credit card statement is generated on the 5th of every month and you pay the bill on the 10th, the bank may report the update at the end of that billing cycle. After the credit bureau processes the update, your CIBIL score may change in the following month.

What Happens When Your Credit Report Shows NH or No History

Some people check their credit score and see NH or No History instead of a number.

This simply means the credit bureau does not have enough data to calculate your score.

Why NH appears

NH usually happens when:

- You have never taken a loan

- You have never used a credit card

- Your credit accounts are very new

Without past credit activity, the bureau cannot evaluate repayment behaviour.

Example

Suppose a 23-year-old student applies for a credit card for the first time. Since there is no previous credit record, the report will show NH.

Once the person starts using credit and making payments, a score is generated after lenders report the data.

What This Means for Loan Approval

Understanding how often CIBIL score is updated is important when applying for loans.

Banks check your latest credit report before approving applications.

Typical score expectations

| Score Range | Meaning |

|---|---|

| 750 and above | Excellent credit profile |

| 700–749 | Good approval chances |

| 650–699 | Moderate risk |

| Below 650 | Higher risk for lenders |

If you recently paid overdue amounts, your score may still show the older data until the next update cycle.

Because of this, many borrowers wait 30–45 days after clearing dues before applying for a loan.

Situations When Your Score May Change Faster

Although updates usually happen monthly, some situations may lead to faster changes.

Possible scenarios

- Loan account closure reported early

- Credit card balance reduced significantly

- Correction of a credit report error

- Lender sending mid-cycle updates

However, these situations are less common.

Common Mistakes People Make About CIBIL Score Updates

Many borrowers misunderstand how the credit system works.

Here are some common mistakes.

Expecting instant score improvement

Paying your credit card today will not change your score tomorrow.

Checking score too frequently

Checking your own score repeatedly does not increase or decrease it. But expecting daily changes leads to confusion.

Applying for multiple loans quickly

Each loan application creates a hard inquiry, which may slightly reduce your score.

Ignoring credit report errors

Incorrect loan entries or late payment records can damage your score if not corrected.

Practical Tips to Improve Your CIBIL Score

Even though the score updates monthly, your financial behaviour matters every day.

Here are practical steps that help.

1. Always pay EMIs on time

Payment history is the biggest factor affecting credit score.

Even one missed payment can reduce the score significantly.

2. Keep credit card usage low

Experts suggest using less than 30% of your credit limit.

Example:

If your limit is ₹1,00,000, try to keep usage below ₹30,000.

3. Avoid unnecessary loan applications

Too many credit inquiries can make lenders think you are financially stressed.

4. Maintain a mix of credit

Having both secured loans and credit cards improves credit profile.

5. Check your credit report regularly

Errors can happen. Reviewing your report helps you detect issues early.

When Should You Check Your CIBIL Score

A good rule is to check your credit score:

- Before applying for a loan

- After clearing loan dues

- When planning a major purchase

- Once every few months for monitoring

Checking it too frequently does not provide much value because the score usually updates only monthly.

FAQ: How Often CIBIL Score Is Updated

Does CIBIL score update every day?

No. CIBIL score does not update daily. Updates usually happen every 30–45 days, depending on when lenders report credit activity.

How long after paying a credit card bill does the score update?

Your score usually updates after the lender reports the payment, which can take around one billing cycle.

Can I request CIBIL to update my score immediately?

No. Credit bureaus cannot change scores unless lenders send updated information.

Why is my CIBIL score not increasing after payment?

The payment may not yet be reported by the bank. Wait for the next reporting cycle.

How long does it take to generate a CIBIL score for new users?

If someone has no credit history, the score may appear after 3 to 6 months of credit activity.

Conclusion

Understanding how often CIBIL score is updated helps avoid unnecessary stress when the score does not change immediately after a payment.

In India, credit scores usually update every 30 to 45 days, depending on when lenders report credit information to credit bureaus. Because of this monthly reporting cycle, improvements in your financial behaviour may take some time to appear in your credit report.

The best approach is to maintain consistent habits like paying EMIs on time, keeping credit usage low, and avoiding too many loan applications.